How To Invest $10K: 7 Best Ways

Maybe you’ve been diligently saving a little every month for a few years, or you’ve recently come into some money you didn’t expect, like a bonus at work. Either way, now you’ve got $10,000 and you want to invest it so you can make even more money.

See more: 5 Things You Must Do When Your Savings Reach $50,000

7 Ways To Invest $10,000

Here are some smart ways to put $10K to work for you.

1. Set Yourself Up

The very first thing you want to do is to make sure you have enough money in your emergency fund. This should be money that accessible — think a savings or money market account — and that will cover you for three to six months if something happens to your income. That way, if you get sick or lose your job, you’ll have something to fall back on as you regroup.

2. Pay Off Debt

This might not be the first thing that comes to mind when you think of investing, but if you’re carrying a balance on your credit cards, paying that off might give you the best return you can get anywhere.

Think about it this way: Suppose you have a $10,000 balance on your credit card and your APR is 25%. By paying off that balance, you’re earning yourself a 25% return. You certainly can’t get that from a CD at the bank, bonds or the stock market.

3. Contribute to Your Retirement Account

If you have a 401(k) at work and you’re not contributing the maximum amount you can — which is $20,500 in 2022, plus a $6,500 catch-up contribution if you’re over 50 — increase your contributions by up to $10,000.

Another option is to contribute to a Roth IRA. If you have a 401(k) at work, you can also contribute to a Roth IRA. The maximum contribution to a Roth IRA is $6,000 per year, plus a $1,000 catch-up contribution if you’re over 50. Note that this contribution limit applies to all IRA accounts — whether Roth or regular — combined. So if you have a traditional IRA and a Roth IRA, you can’t contribute more than the limit to either or both. The 401(k) is a different animal, however, with its own contribution limit.

4. Contribute to an HSA

A Health Savings Account lets you save pre-tax money for medical expenses if you have a high-deductible health insurance plan. You can contribute up to $3,550 if you’re the only one on your insurance plan, or $7,100 if you have a family plan.

The money you put into an HSA grows tax-deferred, and if you withdraw it to pay eligible health care expenses, it’s tax-free. And you can roll it over from one year to the next — all the way up to and into retirement.

5. Buy Series I Savings Bonds

Savings bonds may seem like a boring, old-fashioned investment, but these volatile times show that there is a time and a place for stodgy. And I bonds are not your grandfather’s savings bond. They provide a hedge from inflation because the interest rate is tied to inflation.

Here’s how they work. You can buy up to $10,000 worth of I bonds in a calendar year. The bonds pay interest for 30 years. The interest is based on two rates: a fixed rate for the life of the bond, plus a rate that changes every six months with inflation. The fixed rate and the inflation rate are announced every May 1 and Nov. 1. I bonds purchased between May 1, 2022, and Oct. 31, 2022, are currently paying an annual rate of 9.62% interest.

Interest on I bonds is compounded semi-annually. When you cash in your I bond, you get the principal plus all the interest earned for as long as you’ve had the bond. You must wait one year after buying an I bond to cash it in, and if you cash it in before five years have elapsed, you’ll pay a penalty of three months’ interest.

To purchase Series I Savings Bonds, go to the Treasury Direct website.

6. Ladder Some CDs

Like all fixed interest rates, CD rates are going up. But rates can — and probably will — fall again, and CDs lock in your money for a fixed period of time. The longer the term, the higher the rate, but also, the more risk that rates will rise and you’ll earn less than you otherwise could.

The answer to this dilemma is a CD ladder. To create a CD ladder, you purchase CDs with varying maturities.

For example, with your $10,000, you could buy four $2,500 CDs: a 1-year, a 2-year, a 3-year and a 5-year. When your 1-year CD matures, you can put that money into a longer-term CD if you think interest rates will continue to rise, because you’ll have another CD coming due in another year. When that one matures, you can make the decision about whether to put that money away for the short or the long-term. Because you have some of your money maturing every year or two, you minimize your interest rate risk.

7. Invest in the Market

If you are new to investing, you can start out slowly. If you’re more experienced, you can dive right in. Here are three ways to put your $10K to work for you in the market.

Index Funds

An index fund is a collection of stocks that seeks to replicate an index or an investment benchmark. You can buy an index fund that includes the stocks in the Dow Jones Industrial Average, for example, or the S&P 500. You can also purchase an index fund that has a more narrow focus. For example, you can invest in a fund that tracks the performance of an index of semiconductor stocks or retail stocks.

Index funds are passively managed, which means that investments in the fund are bought and sold only to remain true to the index. An index fund is designed to provide the same return as the index it follows, so it won’t outperform the benchmark.

Many index funds are exchange-traded. Exchange-traded funds, or ETFs, are mutual funds that trade like stocks. This means that their prices change throughout the day, and they typically have very low fees.

Mutual Funds

A mutual fund is a “basket” of stocks, and investors purchase shares of the fund. Because there are different stocks in the basket, a mutual fund provides more diversification than an individual stock. Mutual funds are actively managed, meaning that there is a portfolio manager who watches the fund, buying and selling positions as they see fit.

Individual Stocks

Picking your own stocks entails more risk than buying index or mutual funds, but there is also the potential for greater return. For a new investor, the best advice may come from legendary investor Warren Buffet: Buy what you know. Consider the stocks of companies that make the products you use and, ideally, can’t live without. If it’s a newer product that’s just beginning to take off, so much the better.

If you’re going to invest in individual stocks, you can manage the portfolio yourself with an app like Robinhood or E-Trade, use a discount broker like Fidelity, or you can get some help from a full-service broker like Charles Schwab or Edward Jones. Some firms offer both discount and full-service options.

Keep in mind that you get what you pay for — a full-service broker will cost you more in commissions and fees. In exchange for that cost, you get advice on what to buy, sell and hold.

Final Take

There are lots of things you can do with $10K. You can set yourself up with an emergency fund, put it into a guaranteed safe investment or dabble in the stock market. Whatever you decide to do with your $10,000 in savings, it should be something you are comfortable with and something that furthers your financial goals.

Personal finance book recommendations

Personal Finance Book RecommendationsAs a professional financial advisor, I am often asked for recommendations on books that can help individuals gain a better understanding of personal finance. It is no secret that managing money effectively is a crucial skill that can greatly impact one'

How is the interest on bank deposits calculated?

Interest is the amount of money that a bank pays you for keeping your money in a deposit account, such as a savings account, a fixed deposit, or a certificate of deposit. Interest is also the amount of money that you pay to a bank for borrowing money from them, such as a loan or a credit card.

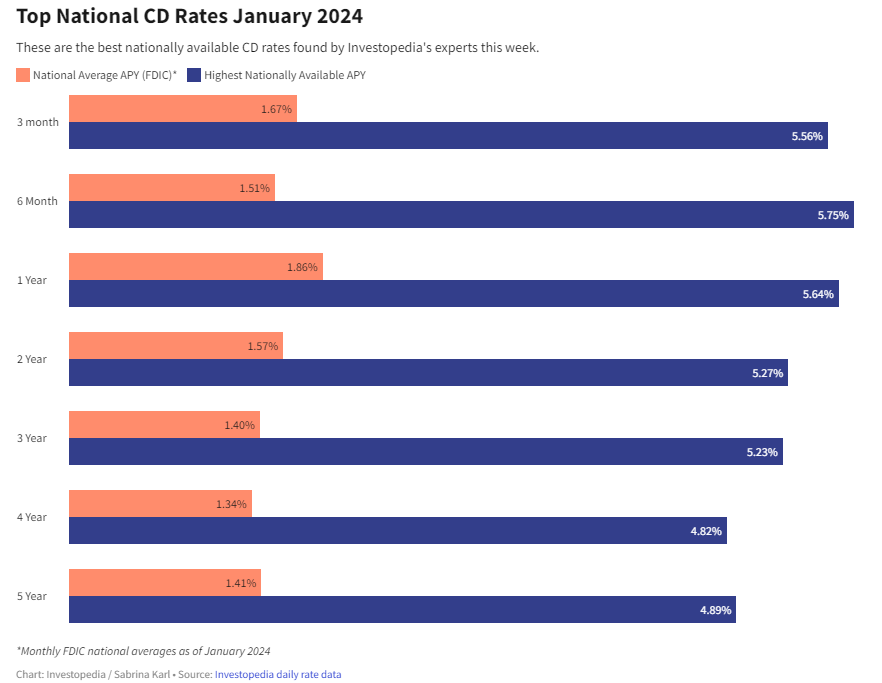

How to Double Your Money with the Best CD Rates for January 2024

If you are looking for a safe and reliable way to grow your savings, you might want to consider opening a certificate of deposit (CD) account. A CD is a type of deposit account that offers a fixed interest rate for a specified term, usually ranging from a few months to several years. Unlike a regula

How to buy the right personal financial products

Personal financial products are tools that help you manage your money, save for the future, and achieve your financial goals. They include things like bank accounts, credit cards, loans, insurance, investments, and retirement plans. However, not all personal financial products are create