Jaspreet Singh: Look at 3 Things To See How Big of a Home You Can Afford

Do you know how much home you can afford? If you don’t know the answer to this question or worry that buying a home may impact your ability to invest and build wealth, personal finance expert Jaspreet Singh shares on YouTube why you should follow an “invest first” rule instead of the bank’s “spend first” rule.

I’m a Real Estate Agent: Don’t Rent an Apartment If It Has Any of These 10 Problems

Read More: 3 Things You Must Do When Your Savings Reach $50,000

Look at these three things to see how big of a home you can buy.

How Much House Can I Afford?

How much of a home you can afford will depend on these three factors.

1. Can You Afford the Monthly Payment?

Answering this question requires building a financial system for yourself where you are always saving and investing your money before you spend it.

Singh recommends following his 75/15/10 rule. For every dollar you earn, 75 cents is the maximum you can spend, 15 cents is the minimum you can invest and 10 cents is the minimum you save. By following this rule, Singh said you’re paying yourself first by investing and saving your money first and spending based on whatever is left. Setting “invest first” parameters means you can adjust your expenses to fit your needs.

Could You Afford a Vacation Home in Europe? Check Out the Prices in These 8 Cities

2. Can You Afford the Down Payment?

“The bigger the down payment, the more skin you have in the game and the less fees you pay,” Singh said.

Those who put down a small down payment when they go out to get a mortgage generally have to pay additional fees, such as PMI costs or other insurance expenses. These fees compensate for additional risks because a smaller down payment is considered a bigger risk for a bank. If a buyer stops paying, they don’t have much skin in the game and face a higher risk of foreclosure.

A buyer who puts down a 20% down payment, however, can avoid these additional fees and save more money on their home. The bigger the down payment, the safer the buyer is in this home. That is, you’re able to experience safety from the chance of foreclosure.

3. Can You Afford the Move-In Costs?

Moving into a new home generally requires upgrading appliances in the home and any interior or exterior designs. Those who don’t account for move-in costs quickly realize it’s expensive to move into a home.

Singh said you don’t want to suddenly go into debt using a 0% APR or buy now pay later (BNPL) to afford all the new things. Furniture is expensive and you want to be sure you’re able to budget for it. Singh recommends setting cash aside for purchasing items like mattresses and working within your “invest first” parameters.

“If you’re going out to buy a home, understand these different costs [monthly payments, down payments you can afford and move-in costs] before you go out and purchase a home,” Singh said.

More From GOBankingRates

Personal finance book recommendations

Personal Finance Book RecommendationsAs a professional financial advisor, I am often asked for recommendations on books that can help individuals gain a better understanding of personal finance. It is no secret that managing money effectively is a crucial skill that can greatly impact one'

How is the interest on bank deposits calculated?

Interest is the amount of money that a bank pays you for keeping your money in a deposit account, such as a savings account, a fixed deposit, or a certificate of deposit. Interest is also the amount of money that you pay to a bank for borrowing money from them, such as a loan or a credit card.

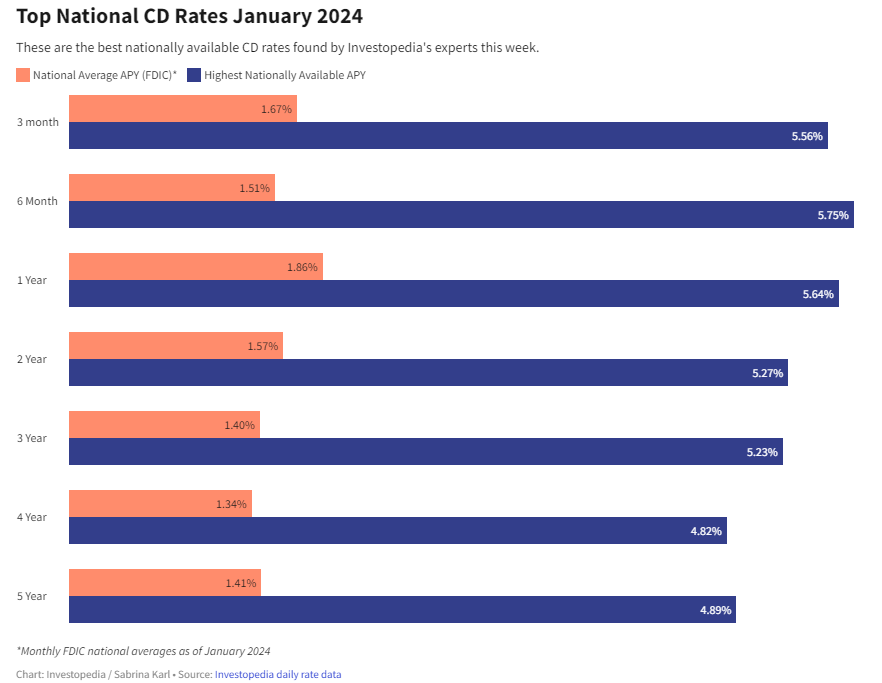

How to Double Your Money with the Best CD Rates for January 2024

If you are looking for a safe and reliable way to grow your savings, you might want to consider opening a certificate of deposit (CD) account. A CD is a type of deposit account that offers a fixed interest rate for a specified term, usually ranging from a few months to several years. Unlike a regula

How to buy the right personal financial products

Personal financial products are tools that help you manage your money, save for the future, and achieve your financial goals. They include things like bank accounts, credit cards, loans, insurance, investments, and retirement plans. However, not all personal financial products are create