Why You Should Keep Your Credit Cards Active

Keeping your credit cards active, even by making one small, monthly purchase, may not seem important. And if you’re digging out of debt or struggling to keep your spending in check, minimizing credit card usage may be the best choice for your overall financial health. Otherwise, consider putting any standard or rewards credit cards that you haven’t used in a while into the rotation for making purchases.

The reason? If your credit card is inactive for a long period — anywhere from about six months to three years, says Ted Rossman, senior industry analyst at Bankrate — the card issuer may close it or reduce your credit limit. That could hurt your credit score.

Why keep your credit cards active?

In order to achieve or maintain a good credit score, you need to monitor your credit-utilization ratio. It’s calculated by dividing your credit card balances (the total amount you owe) by your card limits (both on individual cards and in the aggregate across all your accounts) and reflected as a percentage. Generally, the lower your utilization ratio, the better for your score, and you should try to keep utilization to no more than 30%.

If the available credit on one of your cards is reduced or disappears, the utilization ratio calculated across all of your accounts could increase if you have balances on other credit cards. If your card issuer reduces your credit limit, Rossman suggests asking the issuer to restore it to the previous limit.

Personal finance book recommendations

Personal Finance Book RecommendationsAs a professional financial advisor, I am often asked for recommendations on books that can help individuals gain a better understanding of personal finance. It is no secret that managing money effectively is a crucial skill that can greatly impact one'

How is the interest on bank deposits calculated?

Interest is the amount of money that a bank pays you for keeping your money in a deposit account, such as a savings account, a fixed deposit, or a certificate of deposit. Interest is also the amount of money that you pay to a bank for borrowing money from them, such as a loan or a credit card.

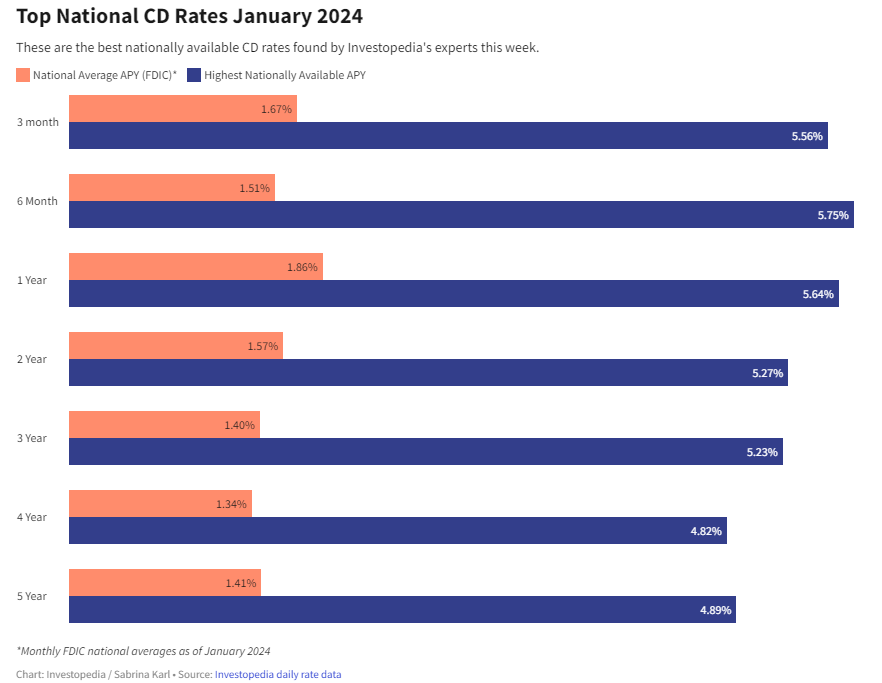

How to Double Your Money with the Best CD Rates for January 2024

If you are looking for a safe and reliable way to grow your savings, you might want to consider opening a certificate of deposit (CD) account. A CD is a type of deposit account that offers a fixed interest rate for a specified term, usually ranging from a few months to several years. Unlike a regula

How to buy the right personal financial products

Personal financial products are tools that help you manage your money, save for the future, and achieve your financial goals. They include things like bank accounts, credit cards, loans, insurance, investments, and retirement plans. However, not all personal financial products are create