Your Retirement Reckoning: Four Questions to Ask

America is facing its great retirement reckoning as millions of workers are close to leaving their day jobs or full-time work and will be confronting important questions to guide their path into a happy retirement and what hopefully will be a healthy new adventure.

The retirement reckoning starts with undeniable demographics. More Baby Boomers will turn 65 next year — what the Alliance for Lifetime Income calls Peak 65 — than at any point in the nation’s history, amounting to about 4.4 million over the course of the year, or more than 12,000 people a day. Most people still retire between 62 and 65, so we are reaching our peak retirement moment. And with the economy somewhere between a rough patch and a recession, even more Boomers may be heading for forced retirement.

Many who transition from their careers see and feel this as a moment of liberation as they prepare to do whatever they choose for their lives instead of working day-to-day out of necessity. For others, it is a time of uncertainty because their daily routine will change, and they haven’t yet settled on what the new normal will be.

For those nearing retirement but not yet ready to take the plunge, or for those who have stopped working but don’t yet feel settled into their new reality, there are four important questions to confront to make the most of this new phase in life:

- What’s the right work?

- Where’s the right place to live?

- Who are the right people to see more frequently?

- What’s the purpose for each day now?

All four questions are interrelated and speak to the need for clarifying what’s next, or what some call the “good life.” The place where you live should provide for the opportunity to be with those most important to you, and whatever new form of work you choose should give you a sense of purpose.

For some, the answers are easy and have been part of their plans and dreams for a long time. They can’t wait to make them a reality.

But my experience is many people have only vaguely considered these questions. In fact, barely half of financial advisers say they have ever talked with their clients about what they want to do in retirement, according to a new survey of advisers by the Alliance for Lifetime Income.(1) Too frequently, advisers simply work from a number the client has provided as to what they think is needed to live on, usually based on their current lifestyle but without taking into account how they actually want to live in retirement.

To help get a meaningful conversation going about how to live the life you want in retirement, here’s a path for making the right decisions:

1. Ask yourself what’s the right type of work for you to be doing now.

Many people will want to supplement their income and transition into partial retirement by continuing to do a form of the job they are doing now, but less of it. Others are ready for something completely different, whether it’s a skill they have never had enough time to use fully or a hobby that can become an enjoyable side hustle.

For those where money isn’t a factor, this is the time for volunteering to help causes that are important to them either by serving on boards or being on the front line of public service.

Part of the answer about work is having a financial plan that takes into account essential and discretionary expenses and being realistic about your needs and desires. This involves determining if you have enough protected income to pay for those essentials, the type of income that comes from Social Security, pension plans and annuity plans.

With financial needs clarified, your decision on what type of work to pursue in retirement also involves knowing what will keep your mind and spirit engaged in meaningful activity and make the days interesting and enjoyable.

2. Who do you want to be near in retirement so you can easily spend time together?

This typically involves family and friends and determining how much is enough time to spend and what may be too much of a good thing. You want to know if what you think makes sense is shared by those you are considering living near. This involves honest and courageous conversations with those you hold most dear. Share what you’re thinking and ask them what they have in mind about where they want to live and what they want to do.

3. Where’s the right place to live?

The work and people considerations will help determine where you should be living. So will cost, health care considerations, weather and lifestyle factors. It’s surprising how many people make a major real estate decision without fully taking those into account.

4. What is your new purpose in this new phase of life?

This can be a hard question to answer. You may want to stretch your current boundaries and try to do something you have never experienced. Learning and exploring are part of the purpose process. So is honestly evaluating your own strengths and willingness to share your time and your gifts.

Personal finance book recommendations

Personal Finance Book RecommendationsAs a professional financial advisor, I am often asked for recommendations on books that can help individuals gain a better understanding of personal finance. It is no secret that managing money effectively is a crucial skill that can greatly impact one'

How is the interest on bank deposits calculated?

Interest is the amount of money that a bank pays you for keeping your money in a deposit account, such as a savings account, a fixed deposit, or a certificate of deposit. Interest is also the amount of money that you pay to a bank for borrowing money from them, such as a loan or a credit card.

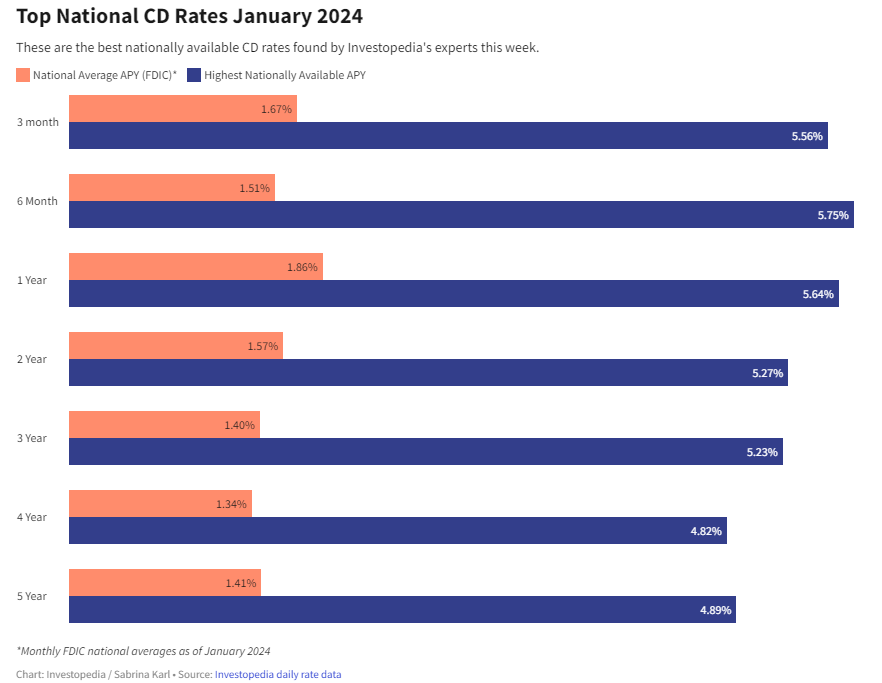

How to Double Your Money with the Best CD Rates for January 2024

If you are looking for a safe and reliable way to grow your savings, you might want to consider opening a certificate of deposit (CD) account. A CD is a type of deposit account that offers a fixed interest rate for a specified term, usually ranging from a few months to several years. Unlike a regula

How to buy the right personal financial products

Personal financial products are tools that help you manage your money, save for the future, and achieve your financial goals. They include things like bank accounts, credit cards, loans, insurance, investments, and retirement plans. However, not all personal financial products are create