If You’re a Baby Boomer Who Retired at 55, How Much Savings Should You Have Left?

Are your retirement savings goals on target? There’s no one-size-fits-all answer, and the age you retire can have a huge impact on the amount you need to save. Retirement experts at Fidelity Investments say that to retire by 67, you need 10 times your income saved. But if you retire at 55, you’ll need much more than that.

See: Most Americans Plan To Spend Less Than $2,000 a Month in Retirement – Are They Being Realistic?

Find: The Simple, Effective Way To Fortify Your Retirement Mix

According to research from the TransAmerica Center for Retirement Studies, the median retirement savings of baby boomers totals $202,000. This may seem like a lot, but based on the 4% rule, this would yield a retirement income of $8,000 per year. On average, U.S. households between the ages of 55 and 64 spend over $78,000 on a variety of expenditures, per data from the Bureau of Labor Statistics.

In an interview with Travel + Leisure, financial wellness educator Danetha Doe said that if you retire at 55, you need enough money saved to cover 20 years or more of living expenses. For example, Doe said she suggests taking your current salary or salary before retirement and multiplying it by 10. If your salary was $80,000 per year, that means you’ll need $800,000 to retire. Over 20 years, this breaks down to $40,000 per year. For some people, this may not be enough, Doe said.

“My suggestion is to use the formula to set a baseline. Then, do research on what it would cost to live the lifestyle you wish to experience in retirement,” Doe explained.

Also: Don’t Claim Social Security Benefits Until You Reach This Milestone

You still have options if you don’t have enough saved to last you throughout retirement.

You can always jump back into the workforce to supplement your retirement income or reduce your expenses as much as possible. You can downsize your home to reduce monthly mortgage payments and property taxes, cut back on subscription services or sell unused vehicles. You can also take advantage of catch-up contributions. The IRS lets savers over the age of 50 make additional contributions to retirement accounts. For 2023, the contribution limit is $7,500.

If you haven’t claimed your Social Security benefits, consider holding off at least until you reach full retirement age. For each month you delay benefits, you increase your benefit amount by a certain percentage. You’ll receive the most if you postpone benefits until age 70.

More From GOBankingRates

Personal finance book recommendations

Personal Finance Book RecommendationsAs a professional financial advisor, I am often asked for recommendations on books that can help individuals gain a better understanding of personal finance. It is no secret that managing money effectively is a crucial skill that can greatly impact one'

How is the interest on bank deposits calculated?

Interest is the amount of money that a bank pays you for keeping your money in a deposit account, such as a savings account, a fixed deposit, or a certificate of deposit. Interest is also the amount of money that you pay to a bank for borrowing money from them, such as a loan or a credit card.

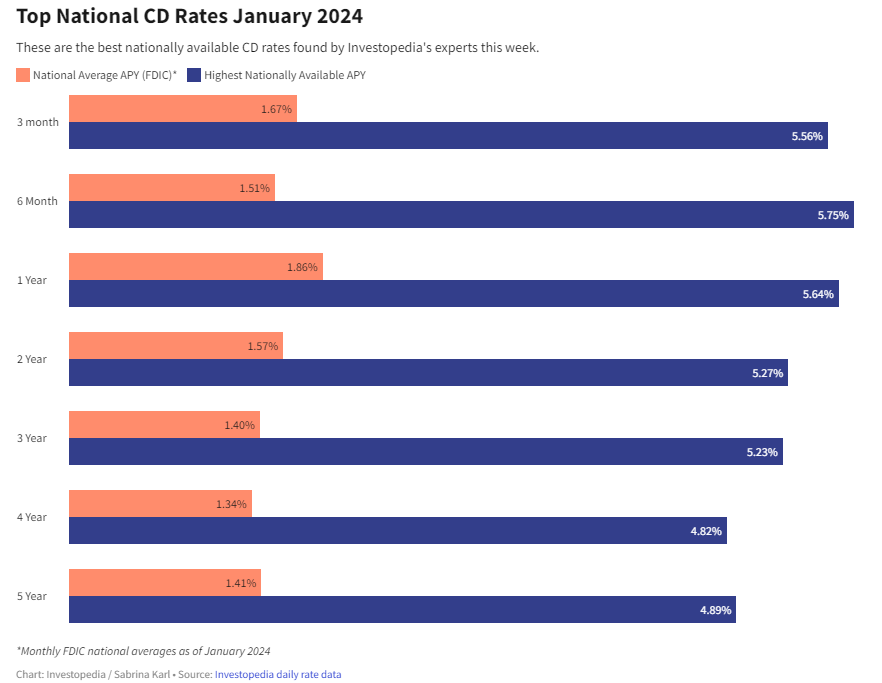

How to Double Your Money with the Best CD Rates for January 2024

If you are looking for a safe and reliable way to grow your savings, you might want to consider opening a certificate of deposit (CD) account. A CD is a type of deposit account that offers a fixed interest rate for a specified term, usually ranging from a few months to several years. Unlike a regula

How to buy the right personal financial products

Personal financial products are tools that help you manage your money, save for the future, and achieve your financial goals. They include things like bank accounts, credit cards, loans, insurance, investments, and retirement plans. However, not all personal financial products are create