3 Investments You Must Make When Your Savings Reach $75,000

When you reach $75,000 in savings, you likely have enough of an emergency fund to cover essentials like housing and food for a few months, said Todd Stearn, founder and CEO of The Money Manual. “So go make your money work for you. If you don’t, inflation will act as a tax that reduces your nest egg each month.”

I’m a Self-Made Millionaire: Here Are 5 Stocks I’m Never Selling

Read More: 3 Things You Must Do When Your Savings Reach $50,000

How? You might be surprised to learn that the best investments to make when your savings near the six-figure mark don’t include the latest hot stock or crypto coin. Here are three solid ways to invest your money once you have $75,000 in savings.

High-Yield Deposit Accounts

For short-term savings — money you plan to use within the next few years — it’s important to keep your funds fairly liquid and protected from loss while earning the best return possible. Stearn recommends putting some of your savings into an FDIC-insured high-yield savings account, money market account or certificate of deposit (CD).

In the past decade or so, these types of accounts paid next to nothing in interest. But since the Federal Reserve started raising its target rate in March 2022, interest rates have been on the rise. Now, you can find deposit accounts that pay 5% APY and up. If you were to put your $75,000 into a one-year CD at 5%, for example, you’d earn $3,750 in interest by the time the CD matures.

Find Out: 5 Things Warren Buffett Says To Do Before a Recession Hits

Debt Payments

If you have outstanding debt, it’s a good idea to focus on paying that off once you have a solid amount of savings. When you have debt, especially high-interest debt, the interest accumulates over time. Every dollar of interest you pay is essentially a dollar lost. By paying off debt more quickly, you gain that money back.

It’s not exactly an investment in the traditional sense, but eliminating debt provides a return on your money. Take this example: Say you have a $20,000 car loan at 8% APR with five years left to repay it. Over the course of those five years, you’d spend about $4,332 in interest. Now say you focused on making extra payments toward your loan and paid it off in two years instead. You’d save $2,623 in interest charges, which would not only be money back in your pocket, but funds available to save or invest instead.

Stearn notes that another valuable side effect of getting rid of your debt is that your credit score will improve. This makes it easier to borrow money at affordable rates, as well as rent an apartment, open utility accounts and even get certain jobs.

Retirement Contributions

Since you have your short-term savings needs taken care of, you can focus on saving for long-term goals. For many people, retirement is a big one. And it’s nearly impossible to save enough money to live off of in your golden years without investing it in the market.

If you have access to an employer-sponsored retirement account, such as a 401(k) or IRA, that’s the best place to start. “These retirement investment products have huge tax advantages,” Stearn said. “The money will multiply over the years.”

Additionally, if your employer matches your contributions, that’s free money. So you should contribute at least the minimum amount required to receive your full employer match.

But it’s important to understand that these accounts are just a place to hold your investments; they’re not the investment itself. You’ll still need to choose the specific stocks, bonds, mutual funds, etc. that you want to invest in, and the options available will depend on your particular plan. Most, however, should give you the option to invest in target-date funds and index funds, which tend to be reliable choices. Still, it can be a good idea to speak with a professional advisor about the best investments that match your risk tolerance and savings goals.

More From GOBankingRates

Personal finance book recommendations

Personal Finance Book RecommendationsAs a professional financial advisor, I am often asked for recommendations on books that can help individuals gain a better understanding of personal finance. It is no secret that managing money effectively is a crucial skill that can greatly impact one'

How is the interest on bank deposits calculated?

Interest is the amount of money that a bank pays you for keeping your money in a deposit account, such as a savings account, a fixed deposit, or a certificate of deposit. Interest is also the amount of money that you pay to a bank for borrowing money from them, such as a loan or a credit card.

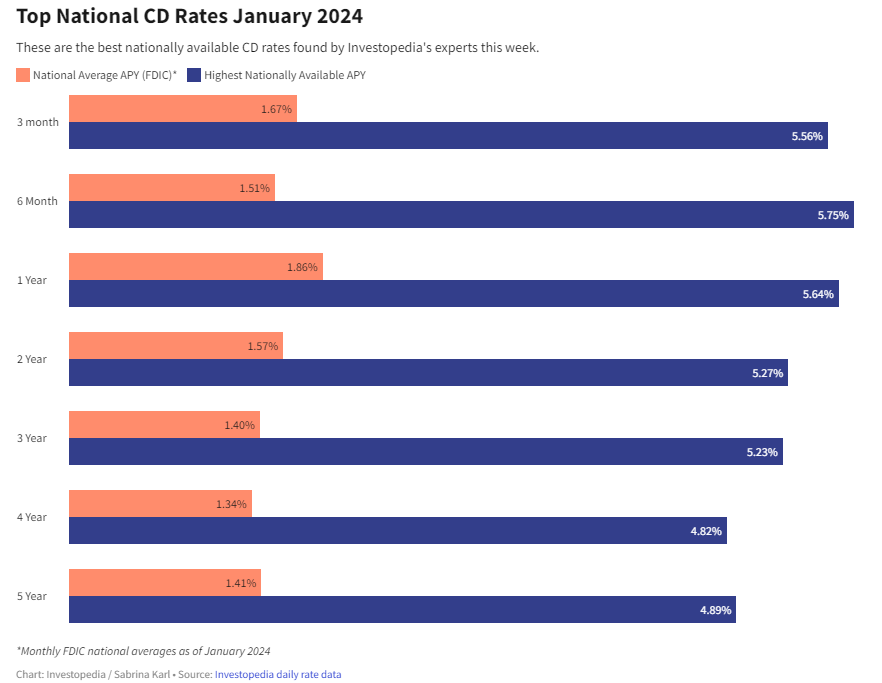

How to Double Your Money with the Best CD Rates for January 2024

If you are looking for a safe and reliable way to grow your savings, you might want to consider opening a certificate of deposit (CD) account. A CD is a type of deposit account that offers a fixed interest rate for a specified term, usually ranging from a few months to several years. Unlike a regula

How to buy the right personal financial products

Personal financial products are tools that help you manage your money, save for the future, and achieve your financial goals. They include things like bank accounts, credit cards, loans, insurance, investments, and retirement plans. However, not all personal financial products are create