Would You Benefit From a Split Interest Income Trust?

The combined marginal tax rate for California residents can now exceed 50%. The residents of Hawaii, New York, New Jersey, Oregon, Minnesota, District of Columbia, Vermont and Iowa all have combined marginal tax rates that exceed 45%.

Taxes on capital gains can take one-third or more of sale proceeds. Every dollar of tax savings that is invested can produce a lifetime return on investments for the family.

Many, but certainly not all, tax planning structures involve charitable structures. This article focuses on an often-missed planning opportunity. The split interest income trust (a version of pooled income fund) provides for the creation of a charitable trust that provides an income tax deduction. When funded, it provides income to you for life (or you may also include your children for their lifetimes) with the remainder going to your designated charity upon the death of the last-named beneficiary.

Here's how a split interest income trust can work

In a real-world example, a father, age 49, with three kids ages 28, 24 and 11, made a $7 million contribution to a split interest intergenerational (includes the kids) income trust. He received an income tax deduction of $2,171,200 and safe annual income for his entire life of $420,000 (projected at 6%) and lifetime income for each of his kids. The father is able to maintain investment control through his own investment adviser and could invest in real estate.

The result is very similar to a charitable remainder trust (CRT). However, the income tax deduction for the split interest income trust is calculated differently than the CRT. The income tax deduction is generally substantially larger for the split interest income trust.

For example, a $1.5 million contribution contributed to a split interest income trust provides a charitable income tax deduction of $983,325 income for his life. This provides yearly tax savings of $324,497 and for his wife’s lifetime of $90,000. The cumulative value of that income after 20 years is $1,040,705. If that was related to the sale of real property or an appreciate, an additional tax savings of $247,500 is possible through bypassing a portion of the capital gain.

Compare that to other charitable remainder trusts

On the other hand, the same $1.5 million contribution to a charitable remainder unitrust (CRUT) would generate a charitable deduction of only $150,000. A CRUT is a charitable trust where a portion of the income is distributed to the family. The amount paid to the family differs each year based on the investment return. The amount remaining at the end of the term or life is paid to the designated charity.

A similar contribution to a charitable remainder annuity trust (CRAT) would generate an income tax deduction of $329,347. A CRAT pays a specified amount to the family for a stated term or for life. The remainder is paid to the designated charity.

The deduction for the CRAT of $329,347 is larger than the $150,000 available for the CRUT. However, both are substantially smaller than the $983,325 charitable contribution available for a comparable split interest income trust.

PIF vs. CRT: What are the differences?

This seemingly too-good-to-be-true alternative is a form of pooled income fund (PIF). Both the PIF and the CRT have been in existence and used since 1969. PIFs are governed under Internal Revenue Code Section 642 (c)(5). CRTs are governed under IRC Section 664. Both PIFs and CRTs generally provide for a donor or the donor’s family to receive economic benefits for a term or lifetime with a remainder interest being distributed to a charitable organization recognized under IRC Section 501 (c)(3).

However, the PIF and the CRT have substantial differences.

The CRT is available in a wide variety of forms, each with unique characteristics. These forms include but are not limited to the CRAT, the CRUT, the net-income CRT, the net income with makeup CRT and the “Flip” CRUT. The holder of the remainder interest must be a charity, preferably a public charity. All CRTs are tax-exempt trusts. This means that a low-basis asset may be contributed for a charitable contribution deductive equal to the asset’s fair market value. That asset can be sold by the CRT tax-free. This enhances the benefit of the charitable contribution, which can be used to offset tax on other assets sold or other income.

The CRT must utilize a minimum payout of at least 5% annually. The CRT planners must make an actuarial calculation imbedded in the trust that creates a remainder investment for charity equal to 10% of the original contribution.

PIFs, while providing a similar result, are very different. There is only one form of PIF, which is not a tax-exempt trust. However, a PIF can receive and sell low-basis assets without recognition of a capital gain. There is no minimum payout and no 10% remainder test, as required for a CRT. While a PIF does require pooling, this requirement can be satisfied by a gift from a husband and a wife, enabling a pool for a single family. There is no minimum age for a PIF income beneficiary. An intergenerational or even multigenerational PIF can be created for two, three or four generations. That is not possible with a CRT.

Personal finance book recommendations

Personal Finance Book RecommendationsAs a professional financial advisor, I am often asked for recommendations on books that can help individuals gain a better understanding of personal finance. It is no secret that managing money effectively is a crucial skill that can greatly impact one'

How is the interest on bank deposits calculated?

Interest is the amount of money that a bank pays you for keeping your money in a deposit account, such as a savings account, a fixed deposit, or a certificate of deposit. Interest is also the amount of money that you pay to a bank for borrowing money from them, such as a loan or a credit card.

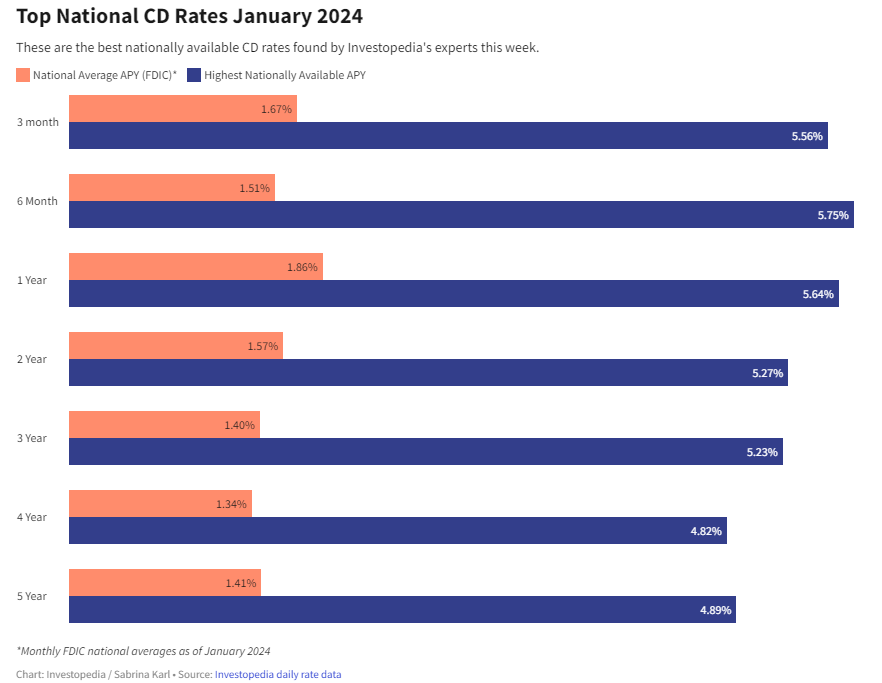

How to Double Your Money with the Best CD Rates for January 2024

If you are looking for a safe and reliable way to grow your savings, you might want to consider opening a certificate of deposit (CD) account. A CD is a type of deposit account that offers a fixed interest rate for a specified term, usually ranging from a few months to several years. Unlike a regula

How to buy the right personal financial products

Personal financial products are tools that help you manage your money, save for the future, and achieve your financial goals. They include things like bank accounts, credit cards, loans, insurance, investments, and retirement plans. However, not all personal financial products are create