The Employee Benefit Choices You Make Now Will Drastically Affect Your Retirement Readiness: 4 Things You Must Know

With open enrollment beginning soon, it’s important to understand your options and the best ways to use the tools available to you to prepare for retirement. Even if you’re still decades away, the decisions you make now can impact your retirement readiness when the time comes.

Read: 5 Places To Retire That Are Just Like Florida But Way Cheaper

Discover: The Simple, Effective Way To Fortify Your Retirement Mix

Here are a few things you should consider when making employee benefits choices to ensure you’ll be retirement-ready.

The ‘One Hour’ Savings Rule: David Bach Says It’s Only ‘Proven, Easy Way To Get Rich’

Beware of ‘Longevity Risk’

Longevity risk — or the risk that you can outlive your savings — is a major financial threat to retirees. Recent research from the TIAA Institute shows that only about a third (35%) of Americans know the average lifespan of retirees, which means that many could be underprepared to fund these years.

“Taking the initiative to start saving for retirement as soon as you’re employed is one of the best hedges against longevity risk,” said Yanelys Benham, wealth management advisor at TIAA. “Too often people wait, and it means they need to either catch up later or simply run out.”

Benham offered the following example to illustrate the importance of starting to save early.

“Let’s say you have two women who both turned 65 last year. The first one started saving for retirement when she was 25. At that point, she set aside $100 a month — just $25 a week.

“The other woman decided to wait 10 more years to start saving for retirement. At that point, she was 35. She waited an extra 10 years, but when she started saving, she set aside twice as much money as the first woman — $200 a month.

“If they both put their money into the S&P 500, then about 40 years later, the woman who started investing when she was 25 would have more than $400,000 because her money had more time to grow. But the woman who waited an extra 10 years? Even though she invested twice as much money once she started saving, her delay means she would have barely $300,000 — a difference of about 25%.”

This is due to compound interest.

“Time is an investor’s greatest asset,” Benham said.

Don’t Overpay and Undersave

If you overpay for health insurance, this means you may end up under-funding your retirement savings plan or health savings account. According to a separate TIAA Institute report, employees who overpay substantially for health insurance are 23% more likely to forgo matching contributions.

“It’s important that everyone evaluates what their health expense needs are for the year, take advantage of the calculators and/or programs to give you guidance on what health plan you should be on, and determine what plan would be the most cost-effective over time based on their needs,” Benham said.

“It’s often difficult to plan what life events may arise that could cause a hefty medical bill, but if over the course of the year you visit the doctor only for your annual check-up, the extra premiums you paid to minimize the cost of a potential hospital visit could have instead been contributed to a health savings account or your retirement account.”

Minimize Your Tax Burden Both While You’re Working and After You Retire

The best way to minimize your tax burden is to save through your employer-sponsored retirement savings plan, such as a 401(k) or 403(b), Benham said.

“For 2023, individuals can contribute $22,500 on a pre-taxed basis, saving them money in taxes today,” she said. “Individuals who are 50 and older can contribute an additional $7,500 per year in employer-sponsored plans. This would be the first place to consider, as many employers offer a matching incentive to contribute to the plan, which you should always take advantage of.”

You may also want to make Roth contributions.

“Many plans have implemented the ability to make Roth contributions to their retirement plan regardless of what their income is, which would receive funds on an after-tax basis and have all the growth tax-free in retirement,” Benham said.

Plan for the Cost of Healthcare in Retirement

To determine how much you need to ensure a comfortable retirement, you must consider your expected healthcare expenditures and start saving for them now. You can do this via a retirement medical savings account or health savings account.

A retirement medical savings account allows you to contribute to the plan on an after-tax basis and allows your investments to grow tax-free if it’s used for healthcare expenses after you turn 65. “In this plan, you could have the funds invested, allowing it to grow over time to cover medical expenses,” Benham said.

A health savings account (HSA) is a plan where you contribute on a pre-tax basis for healthcare expenses either now or in retirement; it’s a plan that can carry forward to the future years.

“Your employer may incentivize you by putting in contributions on your behalf,” Benham said. “Many employers offer a matching incentive to contribute to the plan, wherein a portion of what you put in, up to a certain percentage or dollar amount, is added to the plan from your employer. As a result, not reviewing your benefits and taking time to understand them could mean you’re leaving money on the table that your employer was willing to give to you.”

More From GOBankingRates

Personal finance book recommendations

Personal Finance Book RecommendationsAs a professional financial advisor, I am often asked for recommendations on books that can help individuals gain a better understanding of personal finance. It is no secret that managing money effectively is a crucial skill that can greatly impact one'

How is the interest on bank deposits calculated?

Interest is the amount of money that a bank pays you for keeping your money in a deposit account, such as a savings account, a fixed deposit, or a certificate of deposit. Interest is also the amount of money that you pay to a bank for borrowing money from them, such as a loan or a credit card.

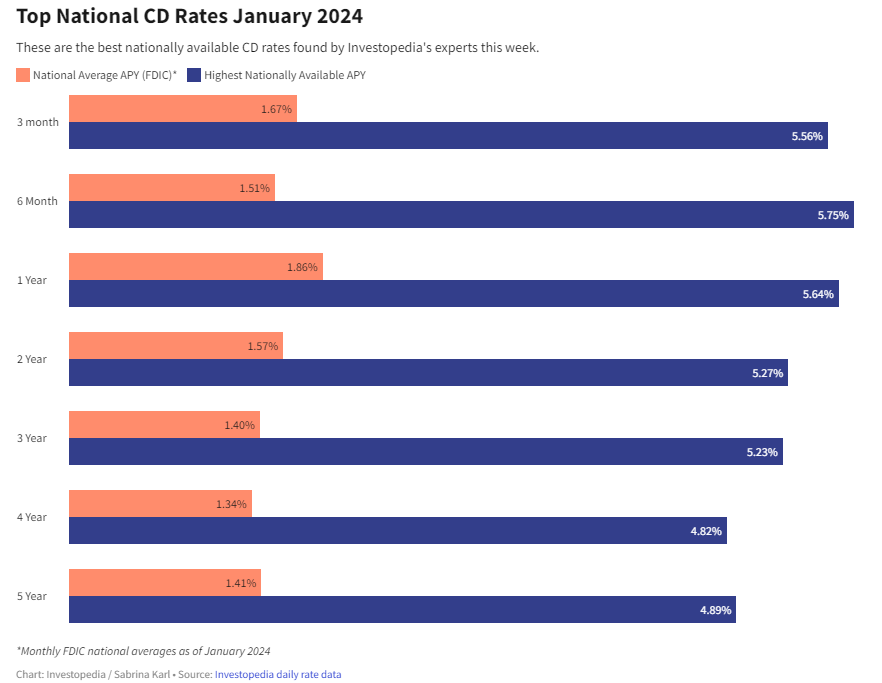

How to Double Your Money with the Best CD Rates for January 2024

If you are looking for a safe and reliable way to grow your savings, you might want to consider opening a certificate of deposit (CD) account. A CD is a type of deposit account that offers a fixed interest rate for a specified term, usually ranging from a few months to several years. Unlike a regula

How to buy the right personal financial products

Personal financial products are tools that help you manage your money, save for the future, and achieve your financial goals. They include things like bank accounts, credit cards, loans, insurance, investments, and retirement plans. However, not all personal financial products are create